Rivalry among existing competitors takes the familiar form of jockeying for position–using tactics like price competition, adver-tising battles, product introductions, and increased customer service or warranties. Rivalry occurs because one or more competitors either feels the pressure or sees the opportunity to improve position. In most industries, competitive moves by one firm have noticeable effects on its competitors and thus may incite retaliation or efforts to counter the move; that is, firms are mutually dependent. This pat-tern of action and reaction may or may not leave the initiating firm and the industry as a whole better off. If moves and countermoves escalate, then all firms in the industry may suffer and be worse off than before.

Some forms of competition, notably price competition, are highly unstable and quite likely to leave the entire industry worse off from the standpoint of profitability. Price cuts are quickly and easily matched by rivals, and once matched they lower revenues for all firms unless industry price elasticity of demand is high enough. Ad-vertising battles, on the other hand, may well expand demand or en-hance the level of product differentiation in the industry for the ben-efit of all firms.

Rivalry in some industries is characterized by such phrases as “warlike,” “bitter,” or “cutthroat,” whereas in other industries it is termed “polite” or “gentlemanly.” Intense rivalry is the result of a number of interacting structural factors.

Numerous or Equally Balanced Competitors. When firms are numerous, the likelihood of mavericks is great and some firms may habitually believe they can make moves without being noticed. Even where there are relatively few firms, if they are relatively balanced in terms of size and perceived resources, it creates instability because they may be prone to fight each other and have the resources for sus-tained and vigorous retaliation. When the industry is highly concen-trated or dominated by one or a few firms, on the other hand, then there is little mistaking relative strength, and the leader or leaders can impose discipline as well as play a coordinative role in the indus-try through devices like price leadership.

In many industries foreign competitors, either exporting into the industry or participating directly through foreign investment, play an important role in industry competition. Foreign competi-tors, although having some differences that will be noted later, should be treated just like national competitors for purposes of structural analysis.

Slow Industry Growth. Slow industry growth turns competi-tion into a market share game for firms seeking expansion. Market share competition is a great deal more volatile than is the situation in which rapid industry growth insures that firms can improve results just by keeping up with the industry, and where all their financial and managerial resources may be consumed by expanding with the industry.

High Fixed or Storage Costs. High fixed costs create strong pressures for all firms to fill capacity which often lead to rapidly es-calating price cutting when excess capacity is present. Many basic materials like paper and aluminum suffer from this problem, for ex-ample. The significant characteristic of costs is fixed costs relative to value added, and not fixed costs as a proportion of total costs. Firms purchasing a high proportion of costs in outside inputs (low value added) may feel enormous pressures to fill capacity to break even, despite the fact that the absolute proportion of fixed costs is low.

A situation related to high fixed costs is one in which the prod-uct, once produced, is very difficult or costly to store. Here firms will also be vulnerable to temptations to shade prices in order to in-sure sales. This sort of pressure keeps profits low in industries like lobster fishing and the manufacture of certain hazardous chemicals and some service businesses.

Lack of Differentiation or Switching Costs. Where the prod-uct or service is perceived as a commodity or near commodity, choice by the buyer is largely based on price and service, and pres-sures for intense price and service competition result. These forms of competition are particularly volatile, as has been discussed. Product differentiation, on the other hand, creates layers of insulation against competitive warfare because buyers have preferences and loyalites to particular sellers. Switching costs, described earlier, have the same effect.

Capacity Augmented in Large Increments. Where economies of scale dictate that capacity must be added in large increments, ca-pacity additions can be chronically disruptive to the industry sup-ply/demand balance, particularly where there is a risk of bunching capacity additions. The industry may face recurring periods of over-capacity and price cutting, like those that afflict the manufacture of chlorine, vinyl chloride, and ammonium fertilizer. The conditions leading to chronic overcapacity are discussed in Chapter 15.

Diverse Competitors. Competitors diverse in strategies, ori-gins, personalities, and relationships to their parent companies have differing goals and differing strategies for how to compete and may continually run head on into each other in the process. They may have a hard time reading each other’s intentions accurately and agreeing on a set of “rules of the game” for the industry. Strategic choices right for one competitor will be wrong for others.

Foreign competitors often add a great deal of diversity to indus-tries because of their differing circumstances and often differing goals. Owner-operators of small manufacturing or service firms may as well, because they may be satisfied with a subnormal rate of re-turn on their invested capital to maintain the independence of self- ownership, whereas such returns are unacceptable and may appear irrational to a large publicly held competitor. In such an industry, the posture of the small firms may limit the profitability of the larger concern. Similarly, firms viewing a market as an outlet for excess ca-pacity (e.g., in the case of dumping) will adopt policies contrary to those of firms viewing the market as a primary one. Finally, differ-ences in the relationship of competing business units to their corpo-ate parents is an important source of diversity in an industry as well. For example, a business unit that is part of a vertical chain of busi-nesses in its corporate organization may well adopt different and perhaps contradictory goals than a free-standing firm competing in the same industry. Or a business unit that is a “cash cow” in its par-ent company’s portfolio of businesses will behave differently than one that is being developed for long-run growth in view of a lack of other opportunities in the parent. (Some techniques for identifying diversity in competitors will be developed in Chapter 3.)

High Strategic Stakes. Rivalry in an industry becomes even more volatile if a number of firms have high stakes in achieving suc-cess there. For example, a diversified firm may place great impor-tance on achieving success in a particular industry in order to further its overall corporate strategy. Or a foreign firm like Bosch, Sony, or Philips may perceive a strong need to establish a solid position in the U.S. market in order to build global prestige or technological credi-bility. In such situations, the goals of these firms may not only be diverse but even more destabilizing because they are expansionary and involve potential willingness to sacrifice profitability. (Some techniques for assessing strategic stakes will be developed in Chap-ter 3.)

High Exit Barriers. Exit barriers are economic, strategic, and emotional factors that keep companies competing in businesses even though they may be earning low or even negative returns on invest-ment. The major sources7 of exit barriers are the following:

- Specialized assets: assets highly specialized to the particular business or location have low liquidation values or high costs of transfer or conversion.

- Fixed costs of exit: these include labor agreements, resettle-ment costs, maintaining capabilities for spare parts, and so on.

- Strategic interrelationships: interrelationships between the business unit and others in the company in terms of image, marketing ability, access to financial markets, shared facil ities, and so on. They cause the firm to attach high strategic importance to being in the business.

- Emotional barriers: management’s unwillingness to make eco nomically justified exit decisions is caused by identification with the particular business, loyalty to employees, fear for one’s own career, pride, and other reasons.

- Government and social restrictions: these involve government denial or discouragement of exit out of concern for job loss and regional economic effects; they are particularly common outside the United States.

When exit barriers are high, excess capacity does not leave the industry, and companies that lose the competitive battle do not give up. Rather, they grimly hang on and, because of their weakness, have to resort to extreme tactics. The profitability of the entire in-dustry can be persistently low as a result.

1. SHIFTING RIVALRY

The factors that determine the intensity of competitive rivalry can and do change. A very common example is the change in industry growth brought about by industry maturity. As an industry matures its growth rate declines, resulting in intensified rivalry, declining profits, and (often) a shake-out. In the booming recreational vehicle industry of the early 1970s nearly every producer did well, but slow growth since then has eliminated the high returns, except for the strongest competitors, not to mention forcing many of the weaker companies out. The same story has been played out in industry after industry: snowmobiles, aerosol packaging, and sports equipment are just a few examples.

Another common change in rivalry occurs when an acquisition introduces a very different personality to an industry, as has been the case with Philip Morris’ acquisition of Miller Beer and Procter and Gamble’s acquisition of Charmin Paper Company. Also, tech-nological innovation can boost the level of fixed costs in the produc-tion process and raise the volatility of rivalry, as it did in the shift from batch to continuous-line photofinishing in the 1960s.

Although a company must live with many of the factors that determine the intensity of industry rivalry—because they are built in-to industry economics—it may have some latitude in improving mat-ters through strategic shifts. For example, it may try to raise buyers’ switching costs by providing engineering assistance to customers to design its product into their operations or to make them dependent for technical advice. Or the firm can try to raise product differentia-tion through new kinds of services, marketing innovations, or prod-uct changes. Focusing selling efforts on the fastest growing segments of the industry or on market areas with the lowest fixed costs can reduce the impact of industry rivalry. Also, if it is feasible a com-pany can try to avoid confronting competitors with high exit barriers and can thus sidestep involvement in bitter price cutting, or it can lower its own exit barriers. (Competitive moves will be explored in detail in Chapter 5.)

2. EXIT BARRIERS AND ENTRY BARRIERS

Although exit barriers and entry barriers are conceptually dif-ferent, their joint level is an important aspect of the analysis of an industry. Often exit and entry barriers are related. Substantial econ-omies of scale in production, for example, are usually associated with specialized assets, as is the presence of proprietary technology.

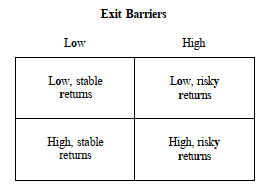

Taking the simplified case in which exit and entry barriers can be either high or low:

FIGURE 1-2. Barriers and Profitability

The best case from the viewpoint of industry profits is one in which entry barriers are high but exit barriers are low. Here entry will be deterred, and unsuccessful competitors will leave the industry. When both entry and exit barriers are high, profit potential is high but is usually accompanied by more risk. Although entry is deterred, un-successful firms will stay and fight in the industry.

The case of low entry and exit barriers is merely unexciting, but the worst case is one in which entry barriers are low and exit barriers are high. Here entry is easy and will be attracted by upturns in eco-nomic conditions or other temporary windfalls. However, capacity will not leave the industry when results deteriorate. As a result capacity stacks up in the industry and profitability is usually chron-ically poor. An industry might be in this unfortunate position, for example, if suppliers or lenders will readily finance entry, but once in, the firm faces substantial fixed financing costs.

Source: Porter Michael E. (1998), Competitive Strategy_ Techniques for Analyzing Industries and Competitors, Free Press; Illustrated edition.