First discussed by the Physiocrats in France, tax incidence is the analysis of the effect of a particular tax on the distribution of economic welfare.

Tax incidence also refers to the ultimate payer of a tax. If a government increases tax on petrol, oil companies may absorb it if competition is intense or they may pass it on to private motorists.

Similarly, a taxi driver may pass on the tax increase to his passenger and a food distributor may pass it on to a supermarket, which in turn passes it on to its customer.

Also see: equal sacrifice theory, ability to pay principle

Source:

J A Pechman, Who Paid the Taxes, 1966-85? (Washington, D.C., 1985)

Tax incidence in competitive markets

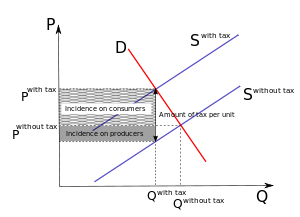

Figure 1 – tax incidence in perfect competition

In competitive markets firms supply quantity of the product equals to the level at which the price of the good equals marginal cost (supply curve and marginal cost curve are indifferent). If an excise tax (a tax on the goods being sold) is imposed on producers of the particular good or service, the supply curve shifts to the left because of the increase of marginal cost. The tax size predicts the new level of quantity supplied, which is reduced in comparison to the initial level. In Figure 1 – a demand curve is added into this instance of competitive market. The demand curve and shifted supply curve create a new equilibrium, which is burdened by the tax.[3] The new equilibrium (with higher price and lower quantity than initial equilibrium) represents the price that consumers will pay for a given quantity of good extended by the part of the tax {\displaystyle (p_{0}+kt),k\in [0,1].}

![{\displaystyle (p_{0}+kt),k\in [0,1].}](https://wikimedia.org/api/rest_v1/media/math/render/svg/db277617a3f625c87df4663ff933773c86fe3b66)

The point on the initial supply curve with respect to quantity of the good after taxation represents the price (from which the part of the tax is subtracted {\displaystyle (p_{0}-(1-k)t),k\in [0,1])} that producers will receive at given quantity. In this case, the tax burden is borne equally by the producers and consumers. For example, if the initial price of the good is $2, and the tax levied on the production is $.40, consumers will be able to buy the good for $2.20, while producers will receive $1.80.

![{\displaystyle (p_{0}-(1-k)t),k\in [0,1])}](https://wikimedia.org/api/rest_v1/media/math/render/svg/1e614728220ddd99b36e24365508ce7de82e9800)

Consider the case when the tax is levied on consumers. Unlike when tax is imposed on producers, the demand curve shifts to the left to create new equilibrium with initial supply (marginal cost) curve. The new equilibrium (at a lower price and lower quantity) represents the price that producers will receive after taxation and the point on the initial demand curve with respect to quantity of the good after taxation represents the price that consumers will pay due to the tax. Thus, it does not matter whether the tax is levied on consumers or producers.[4]

It also does not matter whether the tax is levied as a percentage of the price (say ad valorem tax) or as a fixed sum per unit (say specific tax). Both are graphically expressed as a shift of the demand curve to the left. While the demand curve moved by specific tax is parallel to the initial, the demand curve shifted by ad valorem tax is touching the initial, when the price is zero and deviating from it when the price is growing. However, in the market equilibrium both curves cross.[4]

Income taxes are taxes on the supply of labor (if the income is wages) or capital (if the income is dividends, for example). Corporate income tax incidence is difficult to evaluate because although the direct burden is on corporate shareholders, the tax tends to move capital to be supplied more to non-corporate uses such as housing or partnerships, reducing the return to capital generally, and it moves capital abroad, reducing wages. Thus, in the long-run, once the quantity of capital has adjusted, the incidence is likely on non-corporate capital as much as corporate capital, and much of it may be on labor. Economists’ estimates of the incidence vary widely.[5]

Example of tax incidence

Imagine a $1 tax on every barrel of apples a farmer produces. If the farmer is able to pass the entire tax on to consumers by raising the price by $1, the product (apples) is price inelastic to the consumer. In this example, consumers bear the entire burden of the tax—the tax incidence falls on consumers. On the other hand, if the apple farmer is unable to raise prices because the product is price elastic, the farmer has to bear the burden of the tax or face decreased revenues—the tax incidence falls on the farmer. If the apple farmer can raise prices by an amount less than $1, then consumers and the farmer are sharing the tax burden. When the tax incidence falls on the farmer, this burden will typically flow back to owners of the relevant factors of production, including agricultural land and employee wages.

Where the tax incidence falls depends (in the short run) on the price elasticity of demand and price elasticity of supply. Tax incidence falls mostly upon the group that responds least to price (the group that has the most inelastic price-quantity curve). If the demand curve is inelastic relative to the supply curve the tax will be disproportionately borne by the buyer rather than the seller. If the demand curve is elastic relative to the supply curve, the tax will be borne disproportionately by the seller. If PED = PES, the tax burden is split equally between buyer and seller.

Tax incidence can be calculated using the pass-through fraction. The pass-through fraction for buyers is:

So if PED for apples is −0.4 and PES is 0.5, then the pass-through fraction to buyer would be calculated as follows:

So 56% of any tax increase would be “paid” by the buyer; 44% would be “paid” by the seller. From the perspective of the seller, the formula is:

Elasticity and tax incidence

Compared to previous phenomena, elasticity of the demand and supply curve is an essential feature that predicts how much the consumers and producers will be burdened in the specific case of taxation. As a general rule, the steeper the demand curve and the flatter the supply curve, the more the consumers will bear the tax. The flatter the demand curve and the steeper the supply curve, the more the producers will bear the tax.[6]

Inelastic supply, elastic demand

Because the producer is inelastic, they will produce the same quantity no matter the price. Because the consumer is elastic, the consumer is very sensitive to price. A small increase in price leads to a large drop in the quantity demanded. The imposition of the tax causes the market price to increase from P without tax to P with tax and the quantity demanded to fall from Q without tax to Q with tax. Because the consumer is elastic, the quantity change is significant. Because the producer is inelastic, the price doesn’t change much. The producer is unable to pass the tax onto the consumer and the tax incidence falls on the producer. In this example, the tax is collected from the producer and the producer bears the tax burden. This is known as back shifting.

Elastic supply, inelastic demand

If, in contrast to the previous example, the consumer is inelastic, they will demand the same quantity no matter the price. Because the producer is elastic, the producer is very sensitive to price. A small drop in price leads to a large drop in the quantity produced. The imposition of the tax causes the market price to increase from P without tax to P with tax and the quantity demanded to fall from Q without tax to Q with tax. Because the consumer is inelastic, the quantity doesn’t change much. Because the consumer is inelastic and the producer is elastic, the price changes dramatically. The change in price is very large. The producer is able to pass (in the short run) almost the entire value of the tax onto the consumer. Even though the tax is being collected from the producer the consumer is bearing the tax burden. The tax incidence is falling on the consumer, known as forward shifting.

Similarly elastic supply and demand

Most markets fall between these two extremes, and ultimately the incidence of tax is shared between producers and consumers in varying proportions. In this example, the consumers pay more than the producers, but not all of the tax. The area paid by consumers is obvious as the change in equilibrium price (between P without tax and P with tax); the remainder, being the difference between the new price and the cost of production at that quantity, is paid by the producers.

Special cases

When the supply curve is perfectly elastic (horizontal) or the demand curve is perfectly inelastic (vertical), the whole tax burden will be levied on consumers. An example of the perfect elastic supply curve is the market of the capital for small countries or businesses. In the instance of perfect elasticity of the demand or perfect inelasticity of the supply, the price will remain the same and the entire tax burden is on producers. An example of perfect inelastic supply curve is unimproved land ( it is a need to distinguish the land and the improvements, that might be applied) or crude oil. Thus, the whole tax burden is on landowners and owners of the oil.[4]

The other factors, that might affect the tax incidence is the difference between short-run and long-run and between open and closed economy.

The demand and supply for labor and tax incidence

All factors, which was derived on the tax incidence and competitive market might be used also in the case of market for labor. The key role of the paying the tax burden is still elasticity of the curves. Thus it does not matter, whether the tax is imposed on supplier (households) or companies, which demand the labor as a factor of production. The tax leads to the lower wages and lower employment. However some economists assumes, that supply curve for the labor is backward-bending. It means, that the quantity of labor increases if the wages increase and from given level of the wage it started to decrease. The shape of the curve follows an idea, that high wages is an incentive to work less. So, if the tax is levied of this type of the market, it reduces the wages and therefore the quantity of labor rises.[4]

Tax incidence without perfect competition

A market with perfect competition is very rare. More of the market is said to be imperfect competition such as monopoly, oligopoly or monopolistic competition. Producers choose the level of output, at which marginal cost equals marginal revenue. The demand curve predicts the price level. After taxation, the marginal cost curve shifts to the left to reach a new equilibrium characterized by lower quantity and higher price than before (that is given by the downward slope of the demand curve and marginal revenue curve). Elasticity of the curves is still the essential factor that predicts the size of the tax burden levied on consumers and producers. In general, the steeper the marginal cost curve, the smaller the observed change in output after taxation. The difference between perfect competition and imperfect competition can be observed when the marginal cost curve is horizontal (perfect elasticity). Unlike under perfect competition, when the tax burden will be on consumer, in the case of imperfect competition the supplier and consumer will share the burden. The size depends on the elasticity of demand curve. For instance, if the demand curve is linear, the ratio is balanced half and half). Another difference lies in the ad valorem tax and specific tax. For any given revenue, the output from ad valorem tax will exceed the output from specific tax.[4]

Inelastic supply, elastic demand: the burden is on producers

Similar elasticities: burden shared

Macroeconomic perspective

The supply and demand for a good is deeply intertwined with the markets for the factors of production and for alternate goods and services that might be produced or consumed. Although legislators might be seeking to tax the apple industry, in reality it could turn out to be truck drivers who are hardest hit, if apple companies shift toward shipping by rail in response to their new cost. Or perhaps orange manufacturers will be the group most affected, if consumers decide to forgo oranges to maintain their previous level of apples at the now higher price. Ultimately, the burden of the tax falls on people—the owners, customers, or workers.[7]

However, the true burden of the tax cannot be properly assessed without knowing the use of the tax revenues. If the tax proceeds are employed in a manner that benefits owners more than producers and consumers then the burden of the tax will fall on producers and consumers. If the proceeds of the tax are used in a way that benefits producers and consumers, then owners suffer the tax burden. These are class distinctions concerning the distribution of costs and are not addressed in current tax incidence models. The US military offers major benefit to owners who produce offshore. Yet the tax levy to support this effort falls primarily on American producers and consumers. Corporations simply move out of the tax jurisdiction but still receive the property rights enforcement that is the mainstay of their income.

Other considerations of tax burden

Consider a 7% import tax applied equally to all imports (oil, autos, hula hoops, and brake rotors; steel, grain, everything) and a direct refund of every penny of collected revenue in the form of a direct egalitarian “Citizen’s Dividend” to every person who files income tax returns. The import tax (tariff) will increase prices of goods for all domestic consumers, compared to the world price. This increase in the price of goods will result in two types of dead-weight loss: one attributable to domestic producers being incentivized to produce goods that would be more efficiently produced internationally, and the other attributable to domestic consumers being forced out of the market for goods that they would have bought, had the price not been artificially inflated by the tariff (import tax). The actual cost of the tax will be borne by whichever party (producers or consumers) has the more inelastic demand (see earlier section on relative elasticities), regardless of whether consumers buy domestic or foreign goods, and regardless of where the producers make their goods.[8]

Tax burden of a country relative to GDP

A country or state’s tax burden as a percentage of GDP is the ratio of tax collection against the national gross domestic product (GDP). This is one way of illustrating how high and broad the tax base is in any particular place. Some countries, like Denmark, have a high tax-to-GDP ratio (as high as 48%, the highest in the world). Other countries, like India, have a low ratio. Some states increase the tax-to-GDP ratio by a certain percentage in order to cover deficiencies in the state budget revenue. In states where the tax revenue has gone up significantly, the percentage of tax revenue that is applied towards state revenue and foreign debt is sometimes higher. When tax revenues grow at a slower rate than the GDP of a country, the tax-to-GDP ratio drops. Taxes paid by individuals and corporations often account for the majority of tax receipts, especially in developed countries.[9]

Consumer and producer surplus

The burden from taxation is not just the quantity of tax paid (directly or indirectly), but the magnitude of the lost consumer surplus or producer surplus. The concepts are related but different. For example, imposing a $1,000-per-gallon milk tax will raise no revenue (because legal milk production will stop), but this tax will cause substantial economic harm (lost consumer surplus and lost producer surplus). When examining tax incidence, it is the lost consumer and producer surplus that is important. See the tax article for more discussion.

Effects on the budget constraint

Through the budget constraint might be seen, that uniform tax on wages and uniform tax on consumption have an equivalent impact. Both taxes shift the budget constraint to the left. New line will be characterized by same slope as the initial (parallelism).[4]

Other practical results

The theory of tax incidence has a large number of practical results, although economists dispute the magnitude and significance of these results:

- If the government requires employers to provide employees with health care, some of the burden will fall on the employee as the employer will pass it on in the form of lower wages. Some of the burden will be borne by employer (and ultimately the customer in form of higher prices or lower quality) since both the supply of and demand for labor are highly inelastic and have few perfect substitutes. Employers need employees largely to the extent they can substitute employees for machines, and employees need employers largely to the extent they can become self-employed entrepreneurs. An uneducated population is therefore more susceptible to bearing the burden because they are more easily replaced by machines able to do unskilled work, and because they have less knowledge of how to make money on their own.

- Taxes on easily substitutable goods, such as oranges and tangerines, may be borne mostly by the producer because the demand curve for easily substitutable goods is quite elastic.

- Similarly, taxes on a business that can easily be relocated are likely to be borne almost entirely by the residents of the taxing jurisdiction and not the owners of the business.

- The burden of tariffs (import taxes) on imported vehicles might fall largely on the producers of the cars because the demand curve for foreign cars might be elastic if car consumers may substitute a domestic car purchase for a foreign car purchase.

- If consumers drive the same number of miles regardless of gas prices, then a tax on gasoline will be paid for by consumers and not oil companies (this is assuming that the price elasticity of supply of oil is high). Who actually bears the economic burden of the tax is not affected by whether government collects the tax at the pump or directly from oil companies.

I cling on to listening to the news broadcast talk about receiving free online grant applications so I have been looking around for the best site to get one. Could you advise me please, where could i find some?

Pretty section of content. I just stumbled upon your site and in accession capital to assert that I acquire in fact enjoyed account your blog posts. Any way I will be subscribing to your feeds and even I achievement you access consistently fast.