In this section we describe the decision processes assumed in the model at three different levels of detail. Each description is consistent with the others; they become progressively better defined.

1. A gross description of the model

We assume an n -firm oligopolistic market. Each of the firms is similar in the sense that each makes the same decisions in generally the same way. Variations among the firms are achieved by varying parameters. Thus, in order to describe the model, we specify the internal decision process. Decisions, goals, and departmentalization. Each of the firms makes three basic decisions each time period:

- The price to be charged for the firm’s product is determined. Price is viewed as a decision variable, not simply the direct result of market mechanisms.

- The output to be produced during the next time period is set. Each firm decides how much of the product will be produced over a relatively brief future time period

- A general sales and marketing strategy is chosen. Each firm makes a decision on the amount of sales effort it will exert and the dollar expenditures it will make on sales promotion.

Associated with each of these decisions is a set of relevant goals. Each decision is related (at least in the first instance) with its own set of goals. Decisions within one decision area are made primarily with respect to the immediately relevant set of goals. The major interconnections among goals come through feedback, through expanded search where local goals cannot be achieved, and through certain checks on the feasibility of proposed action.Thus, we have three sets of goals:

- A profit goal. The profit goal is an aspiration level with respect to profits. It is connected most directly with the pricing decision.

- A set of inventory and production goals. The inventory goal is in the form of minimum and maximum limits on inventory size relative to sales. The production goal is a production smoothing objective in the form of constraints on variation in output level. The inventory and production goals are related immediately to the output decision.

- A set of sales goals. The firm has aspiration levels for market share and for The sales goals primarily affect sales strategy. Through interconnections, they also have an important effect on price.

Because the decision process is segmented into three sets of decisions each having its own set of goals, it is convenient to think of each firm as being departmentalized into three subdivisions. These subdivisions -pricing, production, and sales — are relatively independent of each other. Each makes decisions independently, subject to cross-departmental pressures.

Feedback, adaptation, and search. Each firm makes its decisions on the basis of feedback from past results. The firms adjust goals and procedures on the basis of such feedback. Each of the firms uses search to solve problems when problems exist and avoids search when problems do not exist In fact, at the most general level the decision process in each department of each firm can be described as follows:

Obviously, at this level the model is an elaboration of the basic concepts presented in previous chapters.

2. A less gross description of the model

To present the model in more detail, we will describe in this section the decision process followed by each firm in each of the decision areas. In the next major section we will present the details of the actual program.

The output decision. In essence, the firm sets production in response to sales. In the steady state, production in one time period is precisely equal to sales of the preceding time period. However, such a steady state is rather infrequently attained and, when attained, is subject to shocks that make it (except under rare circumstances) transitory. More commonly, the organization seeks to establish a production level that is consistent with a set of changing inventory and production- smoothing goals. The process is indicated in Fig. 8.1.

With respect to inventory, there are two critical values:

- The excess This limit is a size of inventory that leads to complaints from the rest of the organization about the excessive cost of main-taining inventory. The excess limit is a lagged function of sales (becoming larger as sales increase).

Figure 8.1 Output decision.

- The runout limit. This limit is a size of inventory that leads to complaints from the rest of the organization about the loss of sales and sales position due to It is a lagged function of sales.

These two limits define three possible conditions. So long as the inventory lies between the limits, the proposed inventory level will show a small growth of inventory reflecting the aspirations of the inventoryproduction division. If the inventory exceeds the excess limit, proposed in-ventory will be reduced from the previous inventory level. If the inventory is below the runout limit, proposed inventory will be increased.

Proposed production is determined by proposed inventory and a sales forecast, subject to demands for production smoothing. The sales forecast is a simple lagged function of sales. Though described as a forecast, it is a simple summary of past sales data. Proposed production then becomes the forecasted sales plus the difference between proposed inventory and actual inventory. The production- smoothing goal is represented by an upper and lower production limit. If proposed production is within the limits, it is produced. If proposed production is outside the limits, production is set at the limit nearer the proposed level. Normally, the upper production limit is the maximum production in the last π periods (where π is a parameter of the model). Similarly, the lower production limit is the minimum production in the last π periods. However, if production is actually set at a limit, the limit is changed in the direction of the proposed production. Thus, so long as proposed production is within the limits, the limits tend to contract. When proposed production is outside the limits, the limits tend to expand. When a firm has a history of variable production, it is able to allow future variability. Where it has a history of smooth production, it will tolerate rather little variability.

These rules define the output decision. In addition, the inventoryproduction part of the model exerts some pressures on other parts of the system. First, when goals are met, organizational slack is increased. Second, when goals are not met, pressure is put on the sales division to adjust sales to inventory-production needs — that is, to smooth sales by reducing them when proposed production is too high, and by increasing them when proposed production is too low.

The price decision. Price is determined by adjusting present price in the face of feedback on goals, costs, and competitors’ behavior. It is primarily responsive to a comparison between actual profits achieved and the profit goal. It is also sensitive to pressure from sales for price reduction. The process is indicated in Fig. 8.2.

The profit goal exhibits learning at two levels. First, it adapts to actual profits achieved. The goal is a lagged function of profits. Second, the parameters involved in the function change on the basis of experience. We assume two different functions for changing the goal on the basis of experience — one operates when profits achieved exceed the goal, the other when profits are less than the goal. Whenever the goal is achieved without extra search, the firm learns to attend more to recently experienced success. When the goal is achieved after initial failure triggers search activity, the firm learns to attend less to recently experienced failure. When the goal is not achieved even after extended search, the firm learns to attend more to recently experienced failure.

In setting price, the firm first checks three environmental characteristics — costs of manufacture, the effects of past price changes, and competitors’ long-run price behavior. First, if exogenous costs have increased, proposed price is increased proportionately to the change in costs. Second, if profit performance has improved after a prior price change (either up or down) that was induced by a prior profit failure, the price change rule is altered to produce future action more in the direction of the action taken. If the prior action has been followed by a poorer performance, the rule is shifted in the other direction. Thus, “successful” price cuts will stimulate more vigorous price cuts in comparable circumstances; “unsuccessful” price cuts will stimulate less vigorous cuts and possible price raises. Similarly, successful and unsuccessful price raises lead to revision in the rule. Third, the firm also checks the long-run price behavior of competition, specifically of the lowest-priced major competitor. If competition has maintained the same relative price as the firm has, nothing is done. If competition has lowered price proportionately more than the firm, performance on market share and sales goals is checked. If market share is below goal, price is cut to restore the relative price position. If market share is above goal but sales are below, price is cut but only part of the previous relative price position is restored. If both market share and sales goals are being met, price is not changed. If competition has raised price relative to the firm, market share and profit performance are checked. If market share goals are being met, the price raise is followed. If market share goals are not being met and profit goals are being met, nothing is done. If neither goal is being met, price is raised but not as much as the competition’s increase.

Figure 8.2 Price decision.

After these checks are made, the firm considers price from the point of view of profit and sales goals. If profit goals are being met and there is no pressure for price reduction from sales, only internal slack changes. Price is unchanged; organizational slack is increased; sales effectiveness pressure is decreased. If profit goals are not being met and there is no pressure from sales for price reduction, the firm considers its past experience in this situation and raises, cuts, or maintains price according to what has been successful in the past.

Under certain circumstances, however, there will be pressure from the sales division for price reduction. There are two kinds of pressure: the first simply indicates trouble on sales goals; the second (which we might call “emergency” pressure) indicates not only trouble but also a recent adverse change in short-run competitive price position. The feedback on price competition is faster than the feedback routinely checked above. If the firm has achieved its profit goals and the standard pressure is applied, it will cut price somewhat. If emergency pressure is applied, the firm will cut price to restore the previous relative price position. If the firm is not achieving its profit goals, the pressure from the sales division is potentially in conflict with the profit goals. Consequently, there is more resistance to price reduction. If the pressure is of the emergency variety, the firm acts to restore the price position; but it also initiates a search program for other alternatives to price cutting. If the pressure is standard, no price action is taken but the search program is triggered.

The search program consists in the following procedures. They are pursued sequentially (one each time period) until the need for search is removed. (1) Organizational slack is reduced. (2) Inventory excess limit is reduced. (3) Pressure is placed on sales for improved performance. (4) Expenditure for sales promotion is increased. (5) Expenditure for sales promotion is decreased. (6) If all of the other procedures fail, the profit goal is reduced. The order of the search changes in response to experience. If a search procedure is successful (that is, the firm does not search on the next cycle), that procedure goes to the top of the search order list. Whenever a search procedure is unsuccessful, it goes to the bottom of the list. The only exception is the profit goal reduction. Regardless of other changes, it is always the last procedure.

After this, the tentative price is checked against costs to see whether the mark-up is consistent with the profit goal. If it is not, the firm either raises price or cuts costs, depending on past experience.

The sales decision. Since the model is designed to be primarily a model of price and output determination, we have not attempted to build a detailed market strategy decision into it. However, two components of such a decision are made. One decision variable is “sales effectiveness pressure,” which is an index of effectiveness in the sales strategy. It is an aggregate surrogate for decisions that influence sales efficiency. Thus, it can be viewed conveniently as the converse of organizational slack in the sales area. The second decision variable is the percentage of sales revenue used for sales promotion. Though this variable is obviously more operational than the sales effectiveness pressure, it is still an aggregate statistic. Both decision variables directly affect sales; sales promotion expenditures also are a component of costs.

There are three sales goals: (1) An aspiration level with respect to the level of sales; the organization compares its sales level with a sales goal that is a function of recent experience. (2) An aspiration level with respect to market share; the organization compares its market share with a market share goal that is also a function of recent experience. (3) A competitive price goal; the organization does not want its short- run price position relative to competitors to change adversely (i.e., to a higher relative price).

The short-run competitive price goal represents the objectives of the sales force. When relative price position changes adversely, the sales force complains and requests remedial action. Such a feedback is fast. In our model, it is received each time period. Feedback information on the sales level and the market share is somewhat slower. We assume that sales and market share are computed every λSAT and λMST periods respectively.

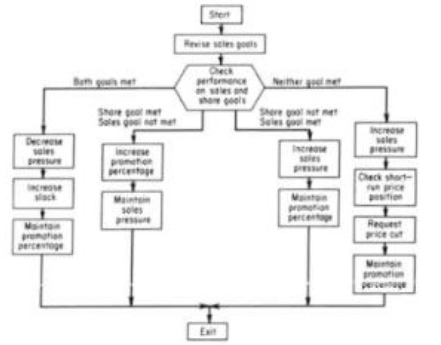

Figure 8.3 shows the sales decision process. The firm checks its sales goals. If the latest report on sales and market share indicates goals have been achieved, the sales department simply continues present policies with an increase in sales slack (i.e., a decrease in “sales effectiveness pressure”) and an increase in general organizational slack. If the market share goal is not being met but the sales goal is, sales effectiveness pressure is increased.

Figure 8.3 Sales strategy decision.

If the market share goal is being met but the sales goal is not, the percentage of sales revenue expended on sales promotion is increased.

If neither market share nor sales goals are achieved, sales effectiveness pressure is increased and the sales department requests remedial price action by the pricing department. If the short-run relative price position has changed adversely, it is an emergency request. If the relative price position has not changed adversely, the request is a standard one (see the pricing program for the difference in reaction to the two types of requests).

Market share and sales goals change at two levels in approximately the same way that profit goals change. Each goal is a weighted average of the previous goal and the immediate past experience. Whenever the goal is achieved, the weights attached to recently experienced success are increased and the weights attached to recently experienced failure are decreased. Whenever a goal is not achieved, the weights attached to re-cently experienced failure are increased while the weights attached to recently experienced success are decreased.

Figure 8.4 Output decision.

3. A least gross description of the model

In this section we indicate the detailed flow charts for the model and discuss the parameters and functional forms introduced. Since such a description is necessarily rather tedious, the reader who wishes to do so may (without excess cost) omit this section.

Detail of the output decision. The detailed flow chart for the output decision is shown in Fig. 8.4. It involves first calculating proposed produc-tion ( PROPRO ) and then checking that proposed production against production- smoothing goals.

Figure 8.4 Output decision (cont.)

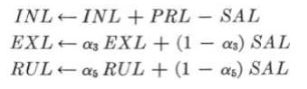

In order to determine proposed production, the inventory-production department determines a proposed inventory level ( INPRO ). First, inventory level ( INL ) is determined by a housekeeping operation — production is added and sales subtracted from the old inventory level to obtain the new one. Second, the program determines the external constraints on the inventory, the excess limit ( EXL ) and the runout limit ( RUL ) by taking a weighted average of the old limits and sales. Thus,

Third, the inventory level is compared with the limits. If inventory is within the limits, the proposed inventory is simply the old proposed inventory times a growth parameter (α 1 ). If inventory is below the runout limit, the proposed inventory increases. The increase is proportional to the differences between the inventory and the limit. Similarly, if the inventory is above the excess limit, proposed inventory represents a decrease that is proportional to the difference between the inventory and the limit. The parameters α 2 and α 4 control the magnitude of change with respect to the excess limit and the runout limit respectively.

The firm then forms a sales forecast ( SFL ) by taking a weighted average of the forecast in the previous period and the sales in the previous period.

![]()

Given the proposed inventory level, the existing inventory level, and the forecast of sales, proposed production is simply that amount of production that will result in the proposed inventory level if the forecast of sales is accurate.

![]()

To determine actual output, we compare the proposed production with the production-smoothing goals. These goals are summarized in the form of an upper production limit ( UPRLIM ) and a lower production limit ( LPRLIM ). The program first checks past performance with respect to the upper and lower production limits. If proposed production was between these limits last time, slack ( SLK ) is increased by α 1. If production has been below the upper limit for π or more times, the upper limit is set equal to the maximum production of the last π periods. If proposed production last time was above the upper limit, we decrease slack, decrease sales effectiveness pressure ( SEP ), and increase the upper production limit. ( SLK and SEP are both indices whose lower bound is 1.)

If production has not fallen below the lower limit for π periods, the lower production limit is set equal to the minimum production for π periods. If proposed production was below the lower limit last time, slack is decreased as above, sales effectiveness pressure is increased, and the lower production limit is decreased:

Having thus determined the production-smoothing goals, we set actual output at the proposed production if this lies between the upper and lower limits. If it violates one of these limits, output is set at the value of the limit.

Detail of the pricing decision. The pricing decision is indicated in Fig.8.5 The firm bases its decisions on three considerations: (1) costs, (2) performance on profit and sales goals, and (3) competitors’ pricing behavior. In a general way, price is maintained unless feedback from one of the three indicates a need for reconsideration of price.

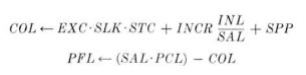

First, every λ PFT periods the firm revises its profit goal and the values of the weights in the profit goal functions. Every period the firm computes its total costs ( COL ) as a function of exogenous costs ( EXC ), slack, sales promotion percentage ( SPP ), and inventory costs ( INCR · INL / SAL ). It then computes a one-period profit level as a function of sales ( SAL ), price ( PCL ), and costs.

Profit total ( PFT ) is a λ period sum of profit level. There are two adjustment functions for the profit goal. If the profit goal ( PFG ) is achieved, the new profit goal becomes a weighted average of the goal and the profit total achieved.

![]()

Similarly, if the goal is not achieved,

![]()

Goal adjustment is subject to the constraint that PFG ≥ 0. If the goal is achieved, ß 1 is increased. This reflects a tendency for the firm to increase attention to its successful performance with each such performance. Similarly, if the goal is not achieved, ß 1 is decreased. The firm learns (through failure) to reduce its attention to recent successes.

If the goal has been achieved, the firm next checks whether that success was preceded by search activity. If it was, it observes whether the success was preceded by a reduction in the profit goal. If so, ß2 is increased, and in the future the firm pays more attention to recent failures in determining profit goal.

![]()

Figure 8.5 Price decision, part 1.

If search has achieved success without reducing the goal, ß2 is decreased. The firm then attends less to recent failures in determining goals.

![]()

Finally, if the profit goal has not been achieved, the firm considers whether it engaged in the search program last period. If so, it revises the search order by moving the unsuccessful search activity to the bottom of the list of search alternatives.

Figure 8.5 Price decision, part 2.

Second, every λ PFT periods the firm also checks exogenous costs. If exogenous costs are up, price is increased proportionately.

![]()

Figure 8.5 Price decision, part 3.

Third, every λ PFT periods the firm checks the results of past adjustments in price designed to improve the profit position. If price has been changed last period in response to a profit failure (see below), the firm asks whether profit has gone up. If it has, ß5 (the parameter controlling the amount of movement in prices) is revised to make future price movements more pronounced in the successful direction. If profit has decreased, ß 5 is revised so as to make future price movements less pronounced in the unsuccessful direction.

If profit is up and ß 5 □ 1: minß 5 ← δ, ß U If profit is up and ß 5 □ 1: minß 5 ← ;4, ß L

Figure 8.5 Price decision, part 4.

Fourth, whenever at least &Ω 1 periods have elapsed since the last price change, the firm considers whether changes in competitors’ prices over a relatively long period require some reaction. In general, a reaction is called for if the long-run relative price position has changed and certain aspiration level conditions are met. If major competitors have increased price relative to the firm’s price and the firm is achieving its market share goal, the price increase will be met. That is, the firm will raise its price to restore the previous price relationship. If competition has raised price and market share goals are not being met, the firm asks whether profit goals are being achieved. If they are, no action is taken. If they are not, the firm raises price but by an amount less than proportional to competition.

![]()

If competition has decreased relative price, the firm again asks whether market share goals are being achieved. If they are not, the decrease is met. If market share goals are being met and sales goals are being met, no price action is taken. If market share goals are satisfied but sales goals are not, the decrease is followed in part (as above).

Fifth, each time period the firm considers its present price in the light of its profit record and pressure from the sales department. If profit exceeds the profit goal, sales effectiveness pressure is decreased and slack is increased.

If price has been changed recently (in &ΩW1 periods), no further action is taken. If price has not been changed recently, the pricing department considers whether there are any price reduction requests from the sales department. If there are no such requests, price is maintained. If there is a standard request, price is reduced.

![]()

If there is an emergency request (and thus a recent short-run change in relative price position), price is adjusted to meet the recent major competitors’ price change and restore relative price position. If profit falls below the profit goal, the department checks for price reduction requests from the sales department. If there are no such requests, if exogenous costs have not just been decreased, and if price has not been changed in the last &Ω 2 periods, the firm will change price in the direction previous experience (ß 5 ) suggests.

![]()

If there is an emergency request for price action, the department meets the recent price reduction by competition. If there is either an emergency or a standard request, or if there has been a recent price change, the firm initiates a search program. In the search routine a series of steps is taken (one each time period) until either profit goals are satisfied or the pressure for a price cut is removed. As we have already noted, the order of the steps of the search routine changes in response to success and failure. There are six possible steps:

Finally, the department checks the consistency of its proposed price, anticipated costs, profit goal, and sales goal. That is, it asks whether the mark-up indicated by comparing price and unit cost will be large enough to meet the profit goal if the sales goal is achieved. If the answer is yes, the proposed price is confirmed. If the answer is no, the firm enters a special search routine. It considers whether it should cut costs or raise price in order to try to make mark-up consistent with goals. If it has most recently cut costs and that strategy succeeded, or if it has most recently raised price and that strategy failed, the department reduces costs by cutting slack and by reducing the sales promotion percentage.

On the other hand, if the department has most recently raised price and that worked or if costs have been cut without success most recently, price is raised so as to be closer to that required to make the goals and mark-up consistent.

![]()

Detail of the sales decision. The sales decision is indicated in Figure 8.6. The decision variables are sales effectiveness pressure ( SEP ) and sales promotion percentage ( SPP ). The major goals are sales, market share, and short- run position.

The program first updates sales and market share goals and the learning parameters associated with them. If a goal is exceeded, the goal is raised, the weight attached to successful performance is increased, and the weight attached to unsuccessful performance is decreased. If a goal is not achieved, the goal is reduced, the weight attached to successful performance is decreased, and the weight given to unsuccessful performance is increased.

Figure 8.6 Sales strategy decision.

The firm then considers where it stands relative to its sales goals. If it is achieving either the market share goal, the sales goal, or both, no request for price action is transmitted to the pricing department. If both goals are being achieved, sales effectiveness pressure is reduced, slack is increased, and promotion expenditures are decreased.

If the market share goal is being achieved but the firm is failing in its sales goal, the proportion of sales revenue invested in sales promotion is increased.

![]()

If the sales goal is met but the market share goal is not, sales effectiveness pressure is increased.

![]()

If neither the sales goal nor the market share goal are met, the department checks recent price competition. If competitors have recently reduced price relative to the firm, an emergency request for price reduction is made. If short-run relative price position is not worse, a standard price reduction request is made.

4. Internal parameters of the model

We can distinguish between parameters of the model that refer to internal attributes of the process by which decisions are made and parameters that are involved in the external environment (e.g., parameters of a demand function). Since we have not yet linked the internal system explicitly to the external environment, we consider here only those parameters referring to the decision process within the firm. In its present form, the model presented has 34 parameters for each firm.

- There are three parameters constraining inventory ( INPROMAX ), production (PROMAX ), and increases in sales (γ 5 ).

- There are eight parameters determining certain lags and lengths of memory in the model: λ SAT, λ MST, and λ PFT, the number of periods covered by aggregate reports on sales, market shares, and profits; π, the number of periods for which past production levels affect current limits on feasible production; &Ω 1, and &Ω 2, the number of periods required to elapse between certain kinds of price changes; Ά 1, and Ά 2, the number of periods for which competitors’ relative price behavior is considered as long run and short run,

- There are fourteen parameters affecting decision variables: α 1, α 2, α 4, and α 6 affect proposed inventory, and thus proposed production; γ 3 and c 1 affect sales effectiveness pressures; ß 3, ß 4, ß U, and ß L affect price; α 10 and α 1 affect organizational slack; γ 4 and γ 6 affect sales promotion percentage. Each of these parameters influences the magnitude of decision reaction to a situation calling for decision change.

- There are five parameters controlling first-level adaptation in the model: α 3 and α 5 affect inventory goals; α 8 and α 9 affect changes in production-smoothing goals; α 11 affects changes in sales forecast.

- There are two parameters dealing with second-level adaptation (or learning): η is the basic parameter in the learning functions for sales, market share, and profit goals; Δ is the increment of change in the price decision rule (ß 5 PCL ) used to correct an unfavorable profit position.

- There are two parameters affecting costs. Standard costs ( STC ) and the inventory cost ratio ( INCR ) enter into the firm’s cost function.

These 34 parameters remain fixed throughout a run of the model. They can be distinguished from another set of internal parameters, the initial values assigned to certain variables in the model. If we treat all of the initial values as independent (which we would not ordinarily do), the model assigns 34 + Ά 1 + π initial values to each firm. Most of these consist in histories of various variables required to overcome the disparity between a no-history firm and the history required by many of the decision rules. Thus, we require a Ά 1- period history of price, an initial slack, an initial sales promotion percentage, an initial upper production limit, an initial lower production limit, a π-period history of production levels, an initial inventory level, an initial excess limit on inventory, an initial runout limit on inventory, an initial sales level, an initial sales forecast, a sales total, a market share total and profit total for the preceding period, an initial sales goal, an initial market share goal, an initial profit goal, an initial market share level, an initial sales effectiveness pressure, initial values for two past price change counters ( W, D ), initial values for the five changing values in the goal and decision rules function (ß 1, ß 2, γ 1, γ 2, γ 5), the firm’s initial relative (vis-à-vis the total industry) sales effectiveness pressure, relative price level, relative promotion expenditure ( RSEP, RPCL, RPEX ), and the initial search routine orders ( SR / T 1, SR / T 2, SR / T 3, SR / T 4, SR / T 5, S, A ).

5. Interactions of the firms in an oligopoly marketplace

In describing our general oligopoly model of price and output, we have thus far concentrated on the model of a specific firm. The entire oligopoly model is made up of n such firms, together with some additional mechanisms that describe the interactions of these firms in the marketplace. Although an identical computer model is used to represent each of the n firms, the initial conditions and internal parameters actually used will in general differ from firm to firm.

There are two major ways in which the n oligopoly firms interact in the marketplace. In the first place, the collective actions of all the firms determine the total level of market demand. In the second place, the individual actions of each firm relative to the collective actions of all firms determine the share of demand that will be generated for each firm. In addition, as we mentioned in our discussion of pricing and sales strategy behavior of a firm, there is one minor way in which the firms interact — namely, the attention which each firm pays to relative price changes vis- à-vis its major competitors (a major competitor being operationally defined as any firm whose market share is at least equal to 1/ n ).

In each time period the total level of market demand (in physical units), which we call DEM, is the following function of the weighted average level of prices set by all firms ( WPCL ), the weighted average level of sales effectiveness pressure for all firms ( WSEP ), the weighted average level of sales promotion expenditures by all firms ( WPEX ), and an exogenous factor ( EXT ):

![]()

Each of the weighted averages in this function uses actual sales level for the previous time period ( SAL ) for each firm as the weighting factor.

The share of market captured by the i th firm ( MSL i ) is a somewhat complex function of its relative sales effectiveness pressure ( RSEP i ), its relative price level ( RPCL i ), its relative promotion expenditures ( RPEX i ) and its previous share of market. (All of these relative measures are vis-àvis the total industry levels of these variables.) The form of this function is as follows ( MSL * i is the ith firm’s un -normalized share of market, MSL i is its normalized share of market):

The level of exogenous cost factors ( EXC ) will change in the marketplace in response to changes in EXT in the following manner:

Thirteen market parameters whose values change over time are introduced here: d 0, d 1, d 2, d 3, d 4, d 5, w 0, w 1, w 2, w 3, w 4, w 5, and w 6. In addition, an initial starting value for EXC must be supplied, together with the entire time series for EXT.

A complete listing of the model in GATE for the Bendix G-20 and one set of sample input and output data are reproduced in an appendix to this chapter. In the case presented some parameter values have been generated by a special GATE random number generation subroutine. To reproduce the results without that subroutine would involve some slight modifications. The only other subroutines used are standard input-output procedures.

Source: Skyttner Lars (2006), General Systems Theory: Problems, Perspectives, Practice, Wspc, 2nd Edition.